Q4 2025 San Francisco Multifamily Report

The San Francisco multifamily market accelerated its recovery in the fourth quarter of 2025, driven by robust transaction volume and tightening supply.

Key market indicators reflect strong positive momentum:

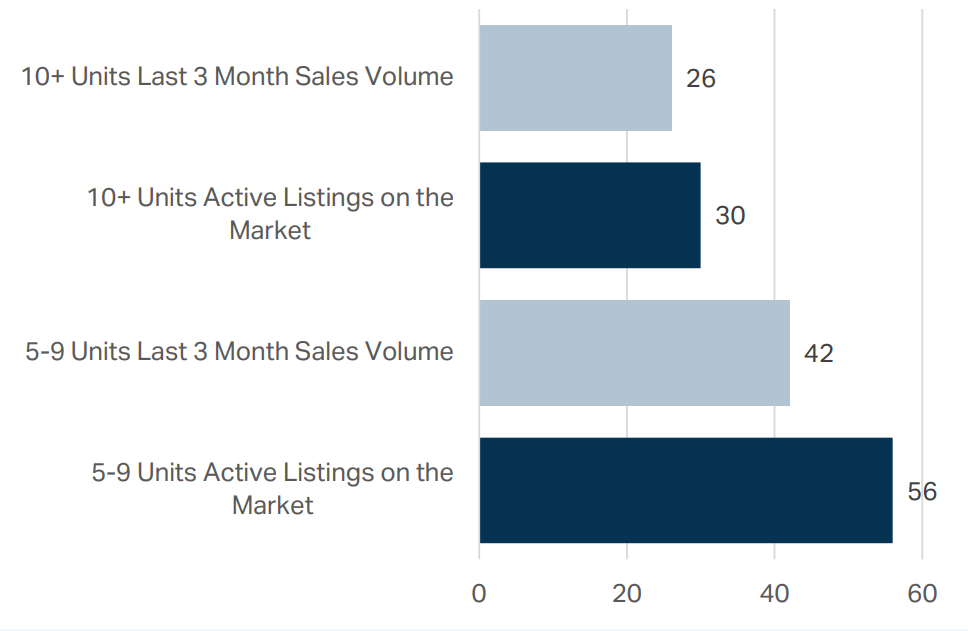

• Absorption accelerated sharply in Q4 2025 versus Q3 last-three-month sales absorbed 87% of current 10+ unit inventory (26 of 30 active listings), up from 49% in Q3 (19 of 39 active); for 5-9 unit properties, absorption rose to 75% (42 of 56 active) from 50% in Q3 (28 of 56 active).

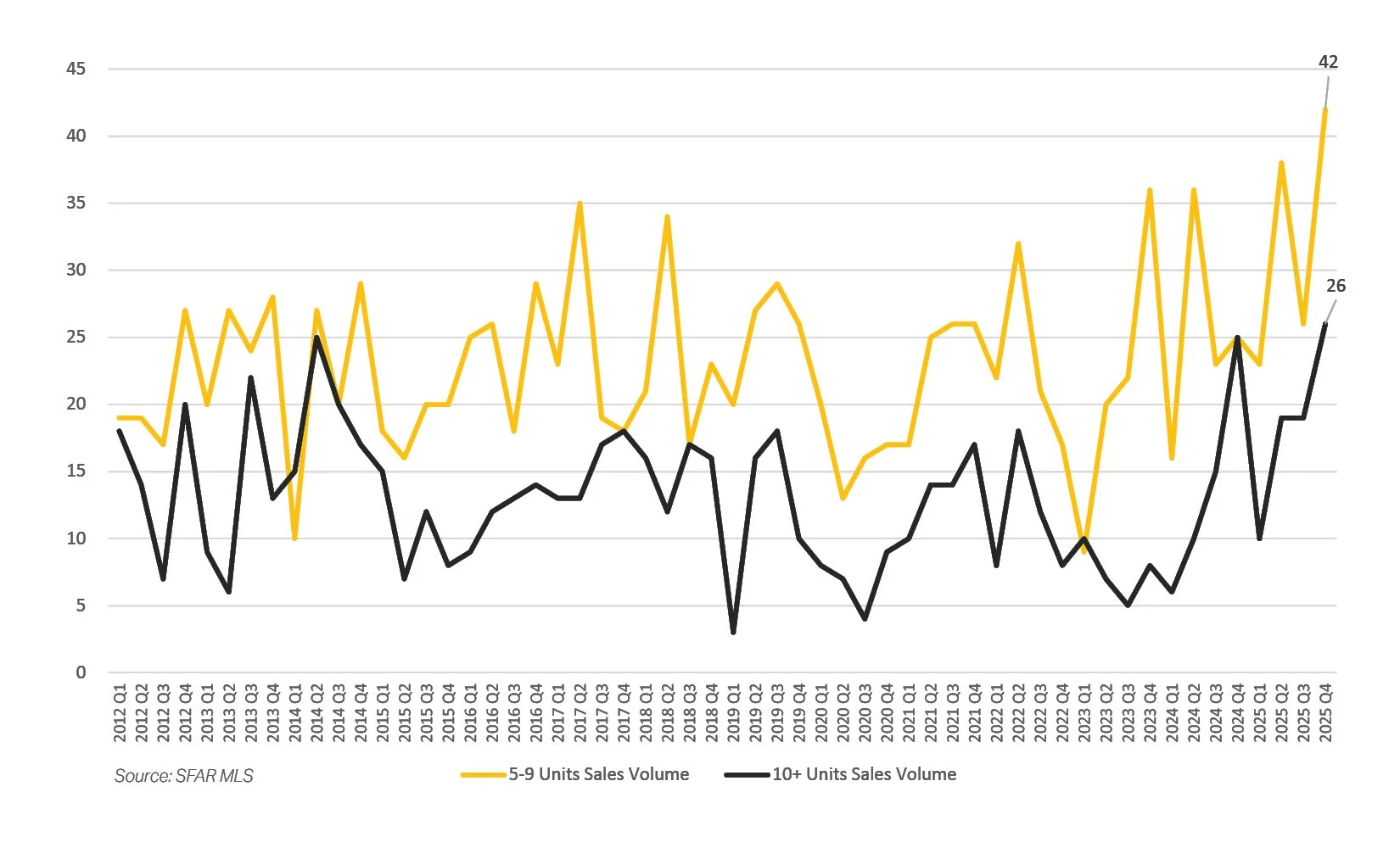

• Sales velocity increased substantially with 26 properties of 10+ units sold in the last three months (up from 19 in Q3 2025) and 42 properties of 5-9 units sold (up from 28).

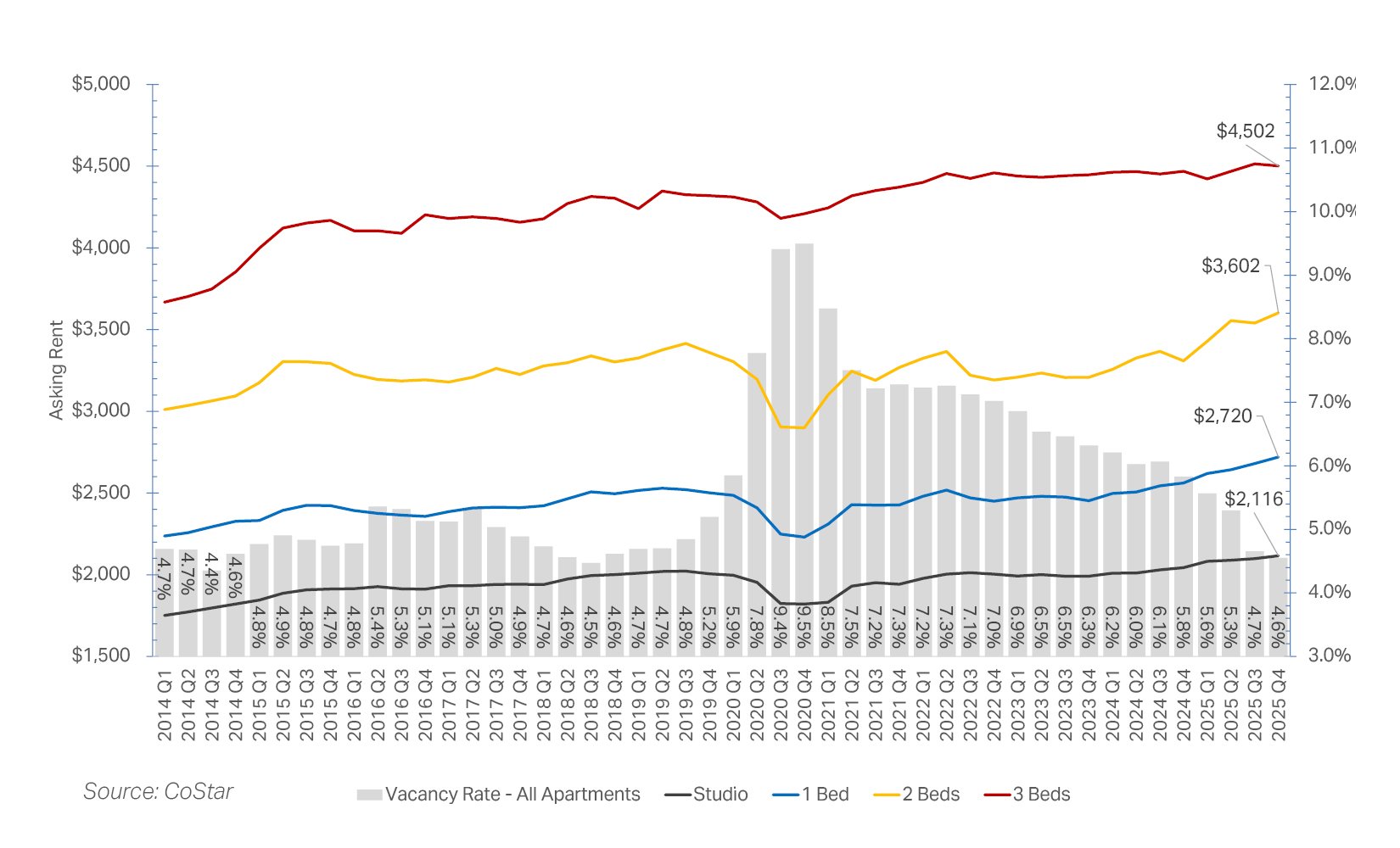

• Effective rents continued their quarter-over-quarter growth amid persistently low vacancy levels.

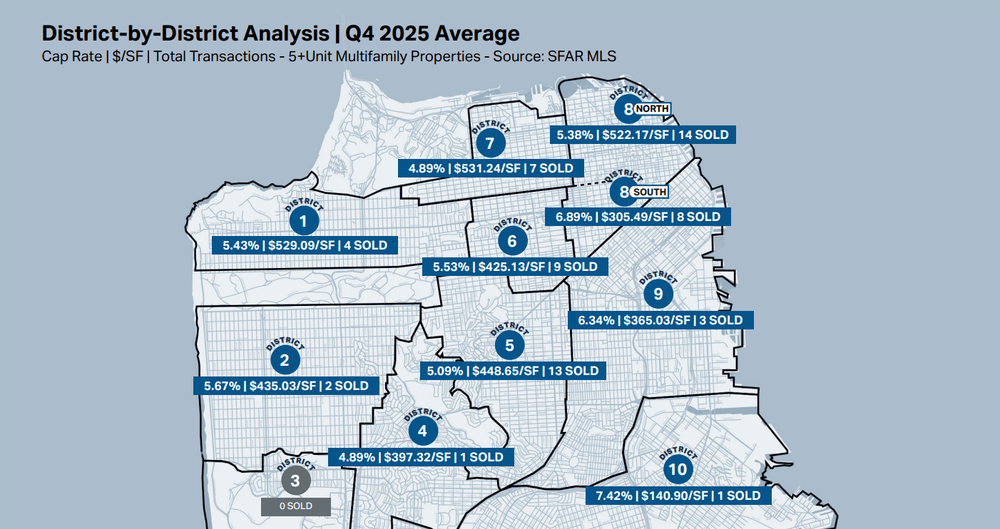

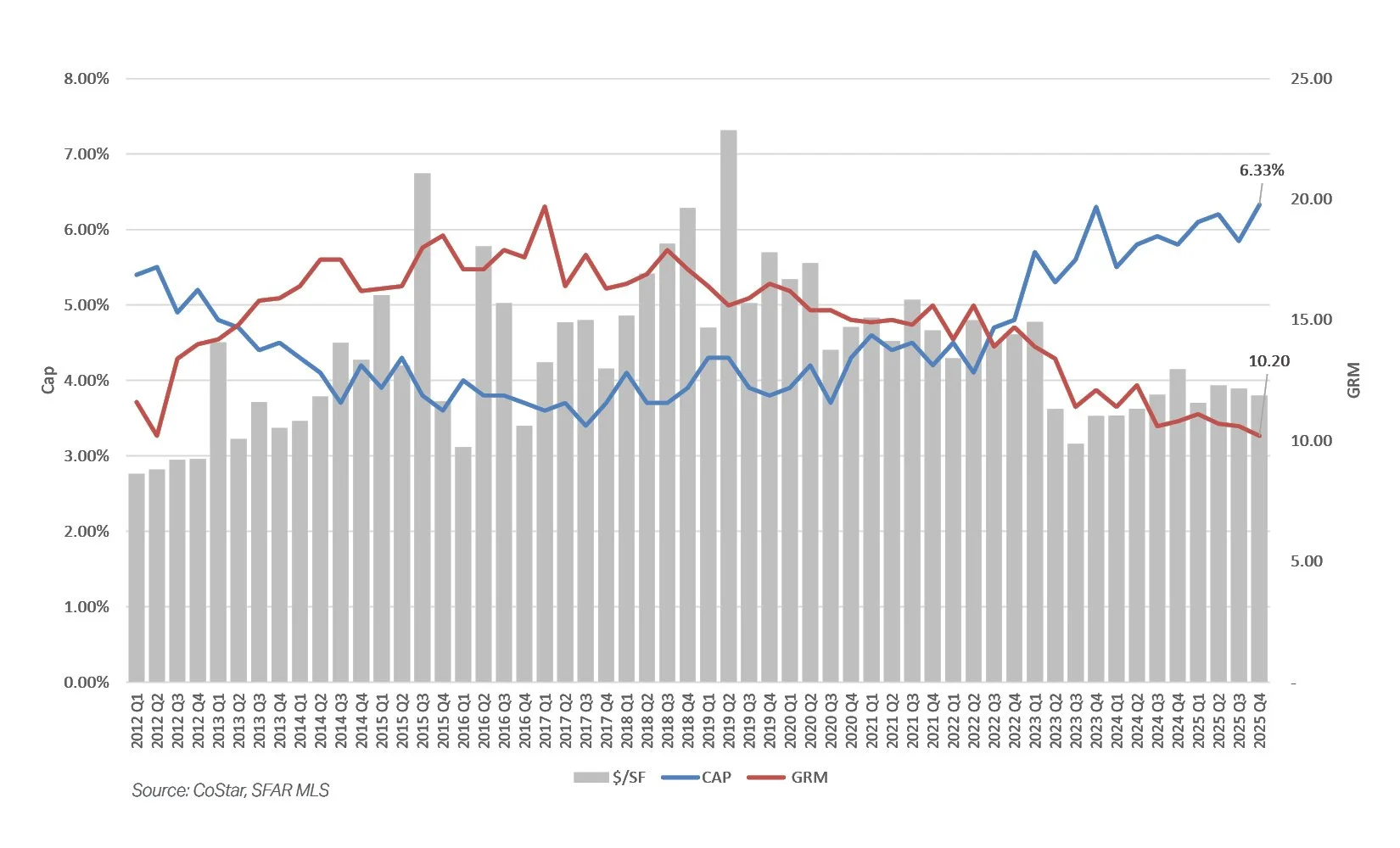

• Cap rates remained competitive with several districts averaging as low as 4.89% and $/SF values reaching $531+ in high-demand areas.

On the ground, LL CRE observed heightened competition with increased tour activity, more aggressive offers terms, and multiple offers becoming increasingly common.

Looking ahead, LL CRE maintains a positive outlook for the San Francisco multifamily sector and anticipates sustained improvement in transaction velocity and pricing through the coming quarters. Competition for quality assets will continue to increase as the buyers in the market consistently increases.

District-by-District Analysis | Q4 2025 Average/Total

Cap Rate | $/SF | Total Transactions - 5+Unit Multifamily Properties - Source: SFAR MLS

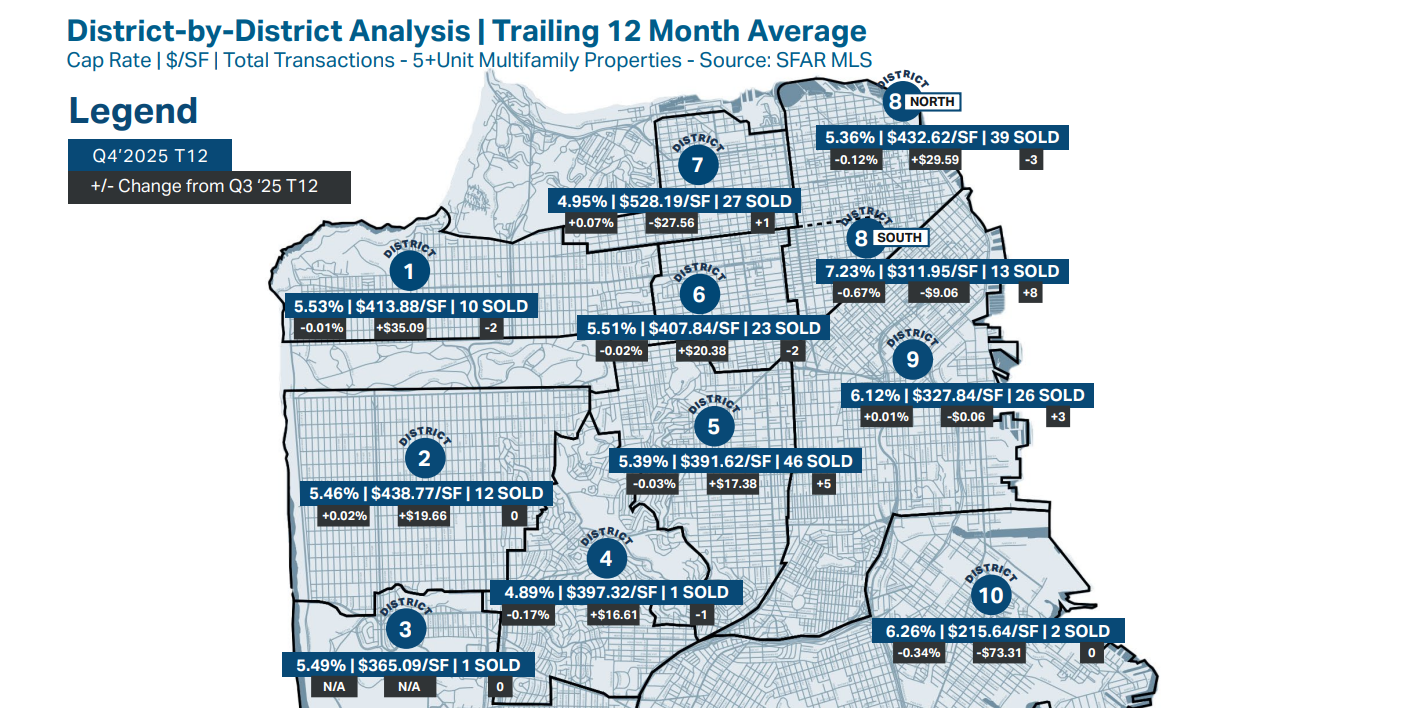

District-by-District Analysis | Trailing Twelve Month Average/Total

Cap Rate | $/SF | Total Transactions - 5+Unit Multifamily Properties - Source: SFAR MLS

Transaction Volume and Active Listings

5+ Unit Properties - Sales Volume

5+ Unit Properties - Average $/SF | Cap Rate | GRM

Multifamily Vacancy Rate & Average Asking Rents

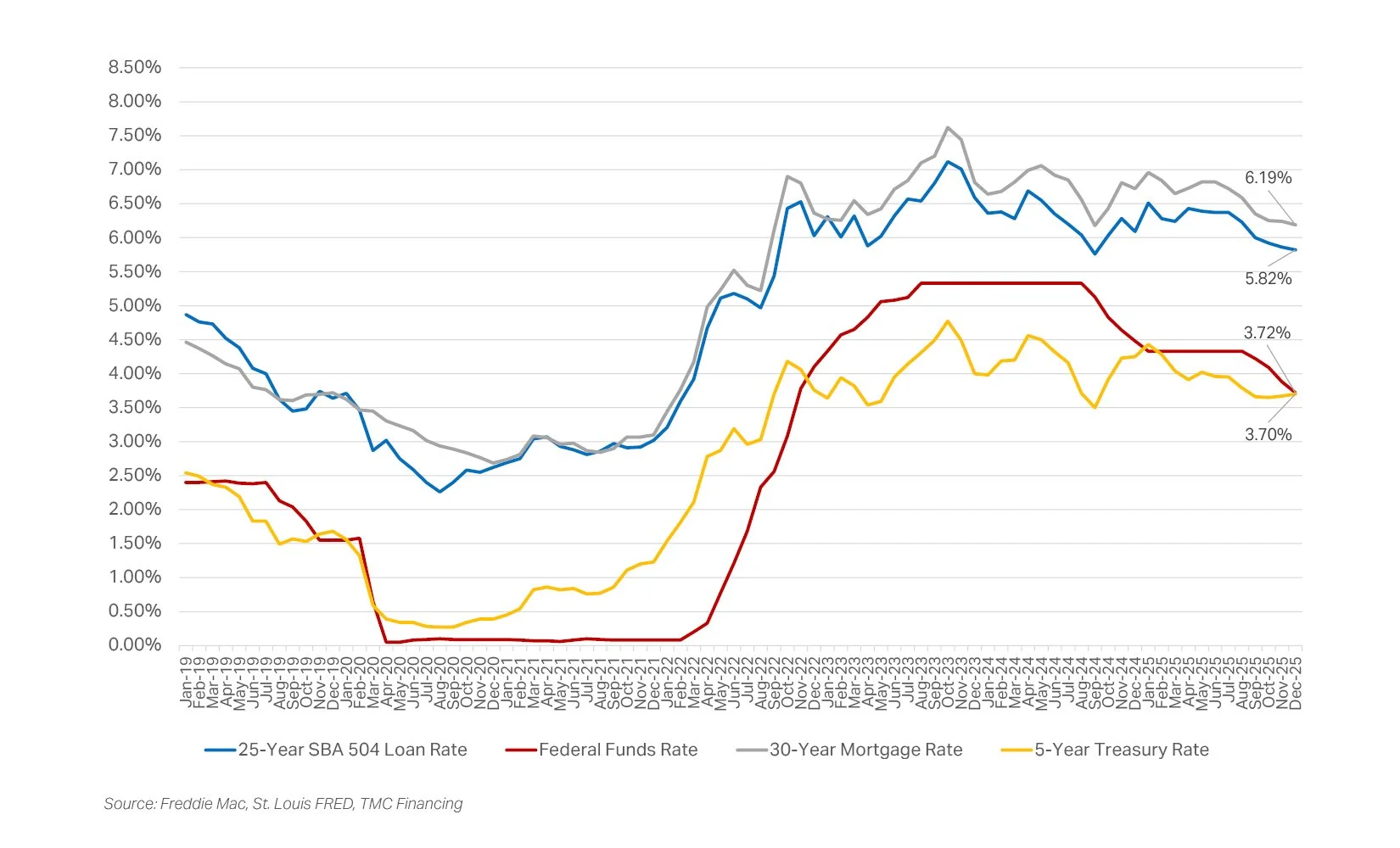

Federal Funds Rate, 30-Year Mortgage Rate,

5-Year Treasury, and 25-Year SBA504 Loan Rate

This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass and LL CRE Group disclaim any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass/ LL CRE Group does not provide such advice. All opinions are subject to change without notice. Compass and LL CRE Group makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.